High Voltage Ahead

U.S. utilities face their first sustained rise in electricity demand in over 20 years, driven by AI data centers and widespread electrification from EVs, automation, and robotics.

U.S. utilities are confronting their first sustained increase in electricity demand in more than two decades. Major cloud service providers (hyperscalers) building data centers for artificial intelligence (AI) workloads, and widespread electrification—such as electric vehicle (EVs), industrial automation and robotics—are all hitting the grid at once. After years of flat electricity demand, could the projected surge in power consumption outstrip current grid capacity, prompting the largest build-out in decades?

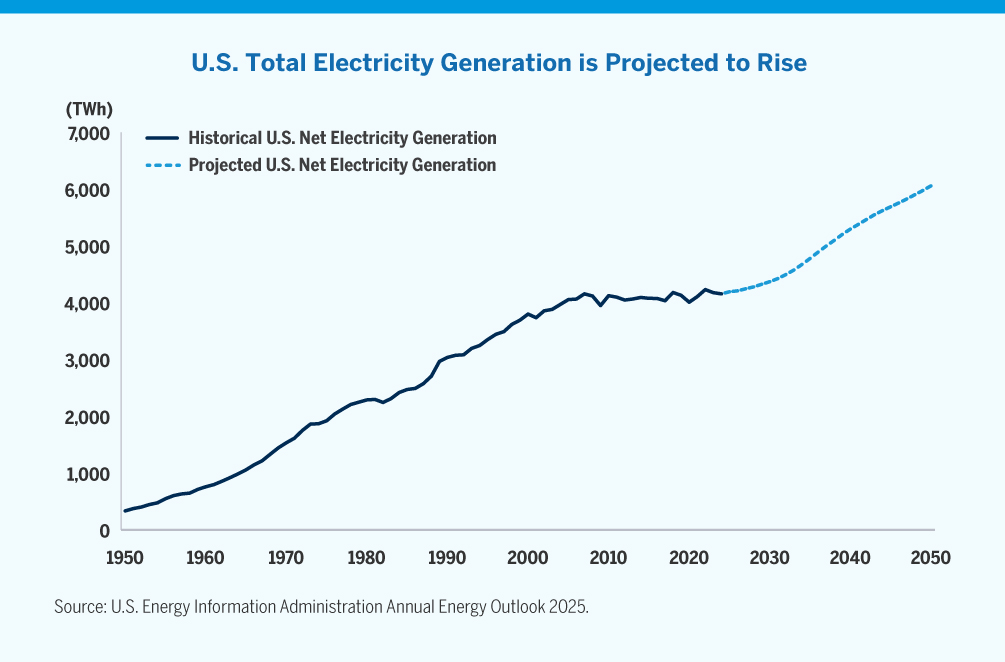

- In the chart above, from 1950 to 2005, U.S. electricity generation soared due to industrialization, suburban development, and widespread adoption of electric appliances. Demand then flattened between 2005 and 2024 when the U.S. shifted to a more service-based economy that outsourced heavy industrial production overseas. However, electricity demand is projected to rise sharply again, spurred by a combination of electrification and data centers running power-intensive AI workloads.1 In fact, over the next five years, U.S. electricity demand is projected to rise at a pace six times faster than it did during the previous five years, requiring additional generation capacity and placing further strain on the nation’s

aging power grid.2

- Data centers are a major contributor to this demand acceleration. Electricity consumption from U.S. data centers alone is projected to climb 133% by 2030—an incremental 243 TWh, enough to power more than 23 million U.S. homes for a year.3 However, meeting surging data center demand hinges on electricity that is

reliable, and quick to bring online. AI hyperscalers are therefore signing long-term power-purchase agreements (PPAs) with independent power producers to secure uninterrupted electricity, predominantly from nuclear and natural gas generation (see also

A Nuclear Energy Renaissance).4

- While data centers may be the most visible growth catalyst in the near-term, we believe the broader U.S. electricity demand wave—industrial automation, EVs and heat pumps—underscores the need for both quick-to-deploy natural-gas turbines and reliably clean baseload power from nuclear facilities over the long term. In our view, companies tied to power generation, transmission, and distribution may be well positioned to benefit from the projected rise in U.S. electricity demand.

1,2 U.S. Energy Information Administration, Annual Energy Outlook 2025. The annual growth rate of U.S. electricity generation from 2019 through 2024 was approximately 0.12%, while the projected annual growth rate from 2025 through 2029 is 0.80%.

3,4 International Energy Agency, World Energy Outlook Special Report 2025

The views expressed are the views of Fred Alger Management, LLC (“FAM”) and its affiliates as of June 2025. These views are subject to change at any time and may not represent the views of all portfolio management teams. These views should not be interpreted as a guarantee of the future performance of the markets, any security or any funds managed by FAM. These views are not meant to provide investment advice and should not be considered a recommendation to purchase or sell securities.

Risk Disclosures: Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Past performance is not indicative of future performance. Investors whose reference currency differs from that in which the underlying assets are invested may be subject to exchange rate movements that alter the value of their investments.

Companies involved in, or exposed to, AI-related businesses may have limited product lines, markets, financial resources or personnel as they face intense competition and potentially rapid product obsolescence, and many depend significantly on retaining and growing their consumer base. These companies may be substantially exposed to the market and business risks of other industries or sectors, and may be adversely affected by negative developments impacting those companies, industries or sectors, as well as by loss or impairment of intellectual property rights or misappropriation of their technology. Companies that utilize AI could face reputational harm, competitive harm, and legal liability, and/or an adverse effect on business operations as content, analyses, or recommendations that AI applications produce may be deficient, inaccurate, biased, misleading or incomplete, may lead to errors, and may be used in negligent or criminal ways. AI companies, especially smaller companies, tend to be more volatile than companies that do not rely heavily on technology.

Important Information for US Investors: This material must be accompanied by the most recent fund fact sheet(s) if used in connection with the sale of mutual fund and ETF shares. Fred Alger & Company, LLC serves as distributor of the Alger mutual funds.

Important Information for UK and EU Investors: This material is directed at investment professionals and qualified investors (as defined by MiFID/FCA regulations). It is for information purposes only and has been prepared and is made available for the benefit investors. This material does not constitute an offer or solicitation to any person in any jurisdiction in which it is not authorized or permitted, or to anyone who would be an unlawful recipient, and is only intended for use by original recipients and addressees. The original recipient is solely responsible for any actions in further distributing this material and should be satisfied in doing so that there is no breach of local legislation or regulation. Certain products may be subject to restrictions with regard to certain persons or in certain countries under national regulations applicable to such persons or countries.

Alger Management, Ltd. (company house number 8634056, domiciled at 85 Gresham Street, Suite 308, London EC2V 7NQ, UK) is authorised and regulated by the Financial Conduct Authority, for the distribution of regulated financial products and services. FAM, Weatherbie Capital, LLC, and/or Redwood Investments, LLC, U.S. registered investment advisors, serve as sub-portfolio manager to financial products distributed by Alger Management, Ltd.

Alger Group Holdings, LLC (parent company of FAM and Alger Management, Ltd.), FAM, and Fred Alger & Company, LLC are not authorized persons for the purposes of the Financial Services and Markets Act 2000 of the United Kingdom (“FSMA”) and this material has not been approved by an authorized person for the purposes of Section 21(2)(b) of the FSMA.

Important information for Investors in Israel: Fred Alger Management, LLC is neither licensed nor insured under the Israeli Regulation of Investment Advice, of Investment Marketing, and of Portfolio Management Law, 1995 (the "Investment Advice Law"). This document is for information purposes only and should not be construed as an offering of Investment Advisory, Investment Marketing or Portfolio Management services (As defined in the Investment Advice Law). Services regulated under the Investment Advice Law are only available to investors that fall within the First Schedule of Investment Advice Law ("Qualified Clients"). It is hereby noted that with respect to Qualified Clients, Fred Alger Management, LLC is not obliged to comply with the following requirements of the Investment Advice Law: (1) ensuring the compatibility of service to the needs of client; (2) engaging in a written agreement with the client, the content of which is as described in section 13 of the Investment Advice Law; (3) providing the client with appropriate disclosure regarding all matters that are material to a proposed transaction or to the advice given; (4) a prohibition on preferring certain Securities or other Financial Assets; (5) providing disclosure about "extraordinary risks" entailed in a transaction (and obtaining the client's approval of such transactions, if applicable); (6) a prohibition on making Portfolio Management fees conditional upon profits or number of transactions; (7) maintaining records of advisory/discretionary actions. This document is directed at and intended for Qualified Clients only.

Alger pays compensation to third party marketers to sell various strategies to prospective investors.

Fred Alger Management, LLC 100 Pearl Street, New York, NY, 10004 / www.alger.com / 800.305.8547 (Retail) / 800.223.3810 (Institutional)