We believe it is time to overcome the psychological inertia of U.S. exceptionalism, reevaluate traditional investment frameworks, and capitalize decisively on the compelling, yet underappreciated opportunities now unfolding in international equities.

Since the 2008 Great Financial Crisis (GFC), the United States has been the world’s most capital-friendly market: the combination of significant monetary and fiscal stimulus, deep capital markets, predictable policymaking, strong adherence to and enforcement of contract law, accommodative labor policy, and reasonable regulation has attracted capital, fueled innovation, and supported premium valuation multiples. This trend also supported the U.S. dollar (USD), as non-U.S. investors deployed substantial amounts of capital into U.S. markets, creating both demand for USD and selling pressure on their local currencies.

Viewed through this same lens, we believe a consequential shift is now taking place outside the United States. The catalysts for this shift are both 1) local political change, with more than 70 national elections in 2024 and record voter participation, and 2) mounting geopolitical strains. Across Europe and Asia, governments are now lowering structural impediments to capital growth, stimulating their economies with fiscal and monetary policy, cutting taxes, streamlining listing requirements, and strengthening corporate governance to drive shareholder value. We believe these actions should spark meaningful investment and unlock new drivers of economic and capital markets growth, just as secular growth engines like energy independence, grid modernization, and artificial intelligence (AI) begin to take off.

Despite these tailwinds, international equities still trade at some of the deepest valuation discounts relative to the U.S. we’ve seen this century. In our view, the disconnect between structurally improving fundamentals and subdued valuations creates an attractive environment for active equity investors. In this piece, we make the case for investing in international equities, focusing on three key drivers:

I. Structural Policy Reforms Are Turning Pro-Growth and Support Profitability: International markets are undergoing a meaningful shift from austerity toward growth-oriented policy and significant capital-market reforms.

II. Emerging Thematic Opportunities Offer Unique Growth Potential: Innovation and technology adoption outside the U.S. are propelling entire industries but remain underappreciated by global investors.

III. Why it Pays to Go Active: The average active international equity manager has historically outperformed passive investing internationally by exploiting persistent and measurable market inefficiencies.

I. Structural Policy Reforms Are Turning Pro-Growth and Support Profitability

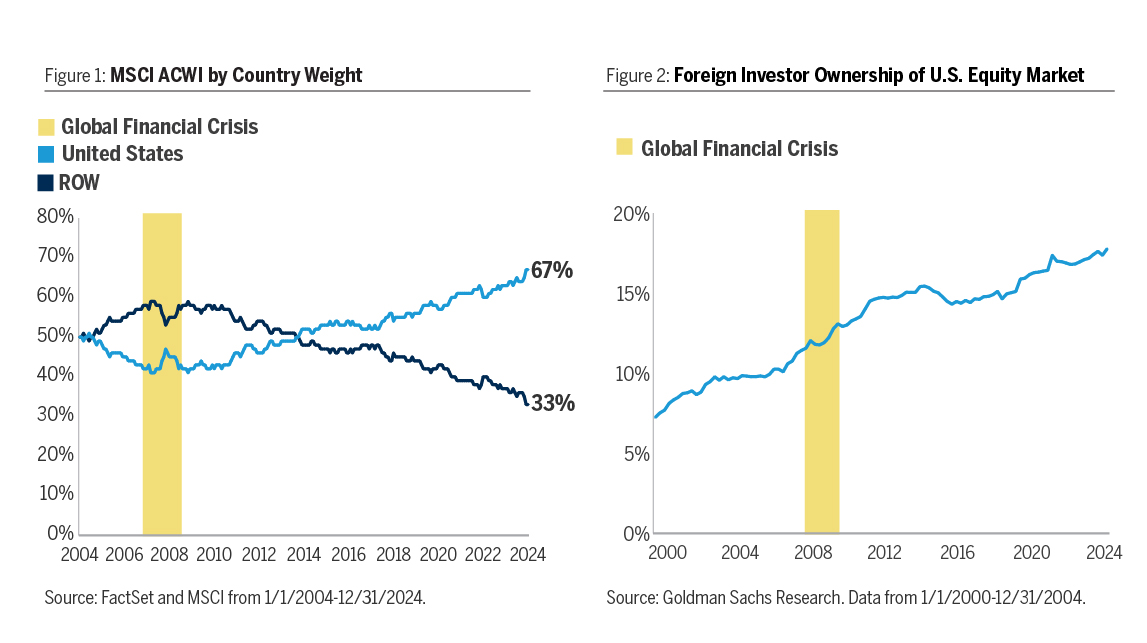

For much of the period following the GFC, the United States enjoyed a deeply entrenched, capital-friendly environment—anchored in efficient capital markets, strong shareholder-oriented governance, a vibrant entrepreneurial culture, low corporate taxes, and innovation-supportive regulation. By contrast, many international economies paired fiscal austerity and higher tax burdens with excessive regulation (e.g., stringent labor laws and costly data-privacy compliance), inadvertently curbing private investment, innovation, and corporate earnings growth. As a result, these last two decades of U.S. outperformance have re-shaped global indices: the United States accounted for approximately 67% of the MSCI All Country World Index’s (ACWI) market value by year-end 2024, up from 42% in 2008 (see Figure 1). Moreover, foreign investor ownership of U.S. equities has increased steadily from 11% at the end of 2007, to 18% in 2024 (see Figure 2). Clearly, investor portfolios have become increasingly U.S.-centric since the GFC; however, the structural pro-growth policies discussed below may be the catalyst to reverse this trend going forward.

Fiscal Policy Pivots from Austerity to Stimulus:

Fiscal Policy Pivots from Austerity to Stimulus: Following the wave of national elections in 2024, governments across Europe, Asia, and Latin America are abandoning post-GFC fiscal austerity and embracing growth-oriented budgets, taking cues from the United States, where deficit-financed investments have delivered superior GDP and equity returns. For instance, Germany has agreed to relax its constitutional “debt brake,” a fiscal rule that traditionally capped its federal budget deficit at 0.35% of GDP—giving the government more room for targeted spending. It also plans to invest €500 billion over the next decade in grid modernization, defense, and digital infrastructure, and offer tax incentives to attract startups and venture capital funding. Japan has matched the pivot with a record ¥115 trillion (~$770 billion) stimulus for automation and capital expenditures (CapEx). China has raised its deficit target to roughly 4% of GDP and is issuing special bonds to fund power infrastructure and advanced manufacturing. India’s 2025 budget allocates ₹11.1 trillion (3.4% of GDP) to roads, rail, and digital connectivity alongside production incentives. Within Latin America, Brazil’s “Novo PAC” channels R$1.7 trillion (~$300 billion) into transportation and energy infrastructure through 2029, while Mexico pairs tax breaks with large shipping port and near-shoring investments. The shared objective: reignite economic growth and corporate earnings.

Monetary Policy Turns Supportive: With inflation moderating throughout the world, central banks in the Euro area, the U.K., China, and several Emerging Markets have begun cutting interest rates, while the Bank of Japan has adopted unprecedented flexibility, allowing yields to settle at levels that still promote credit growth. As of May 31, 2025, among the central banks that implemented rate cuts during the past year are the European Central Bank, the U.K., India, China, Mexico, Korea, and Australia. Importantly, lower real rates reduce the hurdle for investment and should ease the funding cost disadvantage relative to the United States that has long plagued international companies. Meanwhile, persistent U.S. inflation and the Federal Reserve’s (Fed) restrictive monetary policy stance has left U.S. real rates elevated. Paradoxically, a weakening USD from mounting fiscal and trade policy uncertainty could potentially provide an additional tailwind for international equities.

Capital-Market Reforms Unlock Shareholder Value: Across the globe, capital-market reforms are widening access to financing and rewarding shareholders. Japan may be the benchmark for effective corporate governance improvement as the Tokyo Stock Exchange (TSE) reforms push companies to unwind cross-shareholdings and focus on efficient capital deployment—strategic mergers and acquisitions (M&A), research and development (R&D), corporate spin-offs, and return of excess cash to shareholders via buybacks and dividends. In Europe, the Capital Markets Union reboot is under way: Germany’s 2023 Future Financing Act makes it easier for start-ups and small-to-medium sized enterprises (SMEs) to raise capital; France’s Tibi 2 channels institutional money into late-stage technology and health care companies; and Spain is rolling out a flexible initial public offering (IPO) framework and OECD-backed measures to deepen investor participation. Within the emerging markets, China is expanding its registration-based IPO system, easing buyback rules and tightening delisting standards; South Korea’s Corporate Value-Up program couples tax breaks with mandatory value-enhancement plans; India has introduced near-real-time settlement and simplified IPO disclosures; and Saudi Arabia’s Tadawul now permits full foreign ownership and offers new derivatives, broadening sources of capital. In our view, these initiatives are essential to accelerate corporate earnings growth, as they attract global capital, enhance corporate efficiency, and reinforce the foundation for long-term shareholder value creation.

II. Emerging Thematic Opportunities Offer Unique Growth Potential

The U.S. has been the epicenter of corporate growth and innovation for decades, making significant contributions to the personal computer, internet, and smartphone, and potentially leading the world in AI given its momentum in hardware and software development. However, this does not mean that all great growth companies are based in the U.S. In Table 1, we highlight a number of high-growth, secular themes that we believe offer attractive long-term opportunities—and that remain under-represented in most U.S. indices.

E-Commerce and Fintech

| Online shopping is still far less common in India, Southeast Asia, and Latin America than in the United States. Yet rapid smartphone adoption and better logistics give local e-commerce champions a strong tailwind—and a clear path to branch into high-margin financial-services offerings.

|

Neo-Banking and Digital Financial Services

| Underbanked populations and real-time payments reforms are enabling fintechs and progressive banks in Europe, Africa, and emerging Asia to leapfrog legacy infrastructure, and unlock low-cost customer acquisition and fee-based revenue growth.

|

Energy and Power Infrastructure

| Europe’s push for energy independence and grid modernization mandates, and Asia’s AI boom are catalyzing multi-year investment cycles, positioning international utilities, turbine, and power-equipment suppliers for strong, policy-backed earnings growth.

|

E.U. Aerospace & Defense

| Geopolitical re-armament, air-traffic recovery, and supply-chain reshoring are lifting non-U.S. defense budgets and commercial aircraft demand, benefiting European aerospace & defense contractors and diversified international suppliers with high barriers to entry.

|

European Construction Boom

| The E.U. has set aside approximately €1.4 trillion for grid and infrastructure upgrades through 2040, creating long-term demand for builders, engineers, and project managers, while a post-war Ukraine could add another €500 billion in reconstruction work, according to the IMF.

|

Semiconductor Manufacturing & Equipment

| Global chip-capacity expansion, especially in Asia and Europe via policy incentives, secures long-cycle revenue for international foundries and the specialized toolmakers that supply them. Taiwanese and Korean manufacturers have taken the lead from U.S.-based suppliers of cutting-edge chips.

|

Biopharma

Manufacturing

| Global pharmaceutical companies are increasingly outsourcing drug and vaccine production to Europe and emerging Asia, providing international Contract Development and Manufacturing Organizations (CDMOs) with potentially significant volume growth and margin improvement. Meanwhile, recent acquisitions of U.S.-based CDMOs have reduced available manufacturing capacity within the U.S.

|

Super Apps

| A super app is a single mobile platform that combines messaging, payments, commerce, and other everyday services to create a powerful digital ecosystem that boosts user engagement and revenue through network effects. In our view, international markets with limited brick-and-mortar retail, high cash usage, and large unbanked populations offer ideal conditions for super-app development.

|

Addressing Myopia and Vision Technology

| According to the American Academy of Ophthalmology, myopia—or nearsightedness—will rise from 40% of the global population, roughly 3.2 billion people today, to 60% by 2050. Additionally, we believe the gradual integration of connected glasses (i.e., internet connectivity) with AI and audiological technology may have a substantial total addressable market.

|

Beyond energy independence, Russia’s invasion of Ukraine also exposed the scale of Europe’s under-investment in defense. Since 2022, NATO countries outside the U.S. have added over €150 billion to annual defense budgets, and most are legislating multi-year outlays to reach or exceed the 2%-of-GDP target—fueling demand for aerospace, cybersecurity, and other dual-use technologies. At the same time, governments worldwide now treat advanced compute and AI infrastructure as critical assets, steering capital toward domestic chip fabrication, cloud capacity, and AI-software ecosystems rather than relying solely on U.S. or Chinese platforms. Together, we believe these energy, defense, and technology priorities embed long-duration spending into national frameworks, and create powerful secular tailwinds for companies that enable sovereign security in both the physical and digital realms.

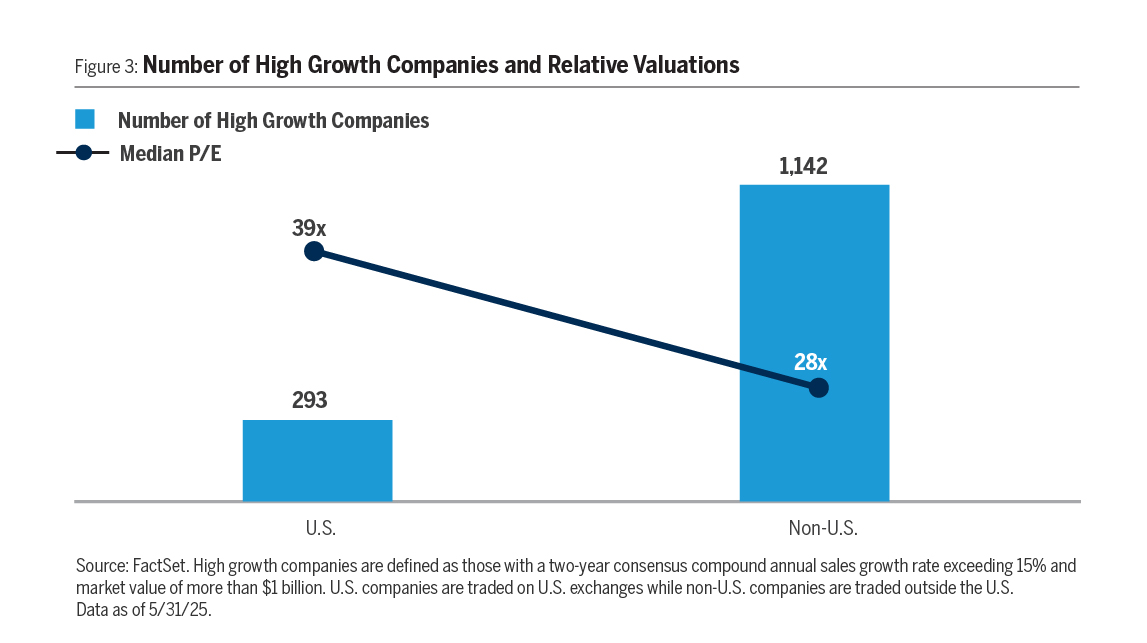

International Growth Stocks at Lower Valuation Multiples: The previously discussed themes are only a fraction of the opportunities outside the U.S. In fact, there are nearly four times as many high-growth companies–defined as those with two-year consensus sales growth exceeding 15% annually—trading outside the U.S. as there are within (see Figure 3). Moreover, valuations for high-growth stocks outside the U.S. appear quite attractive, with a median price-to-earnings ratio that is 28% lower than their U.S. peers.

Attractive Valuations Amplify Opportunities:

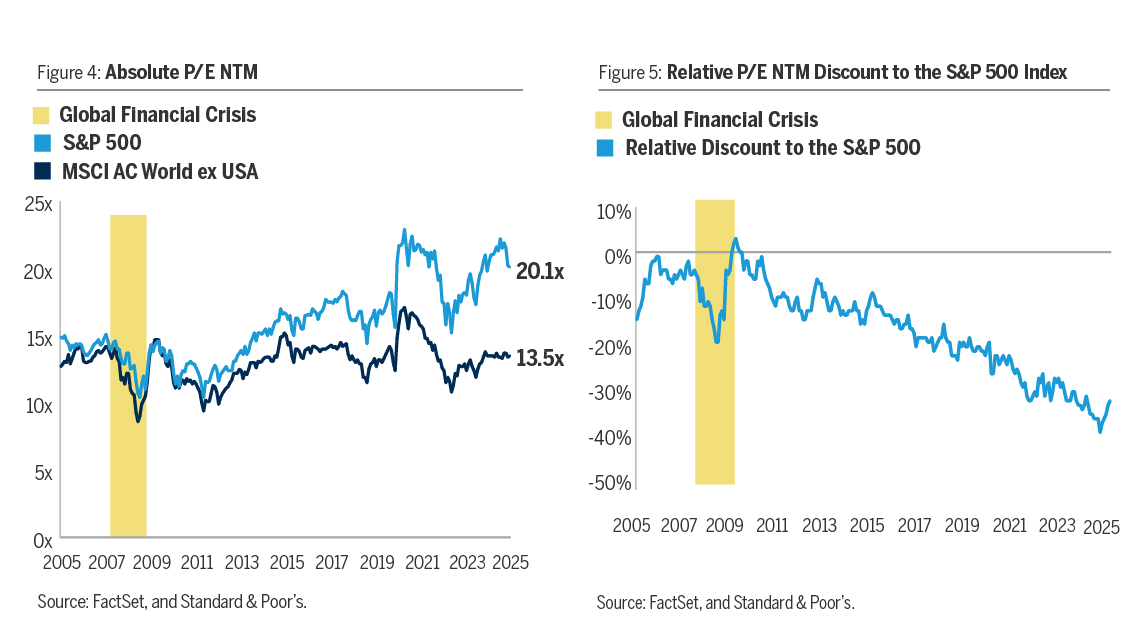

Attractive Valuations Amplify Opportunities: An investment case built on policy reforms and improving growth prospects outside the U.S. is enhanced by attractive valuations: today’s international equity valuations offer some of the widest historical discounts relative to the U.S. (see Figures 4 and 5).

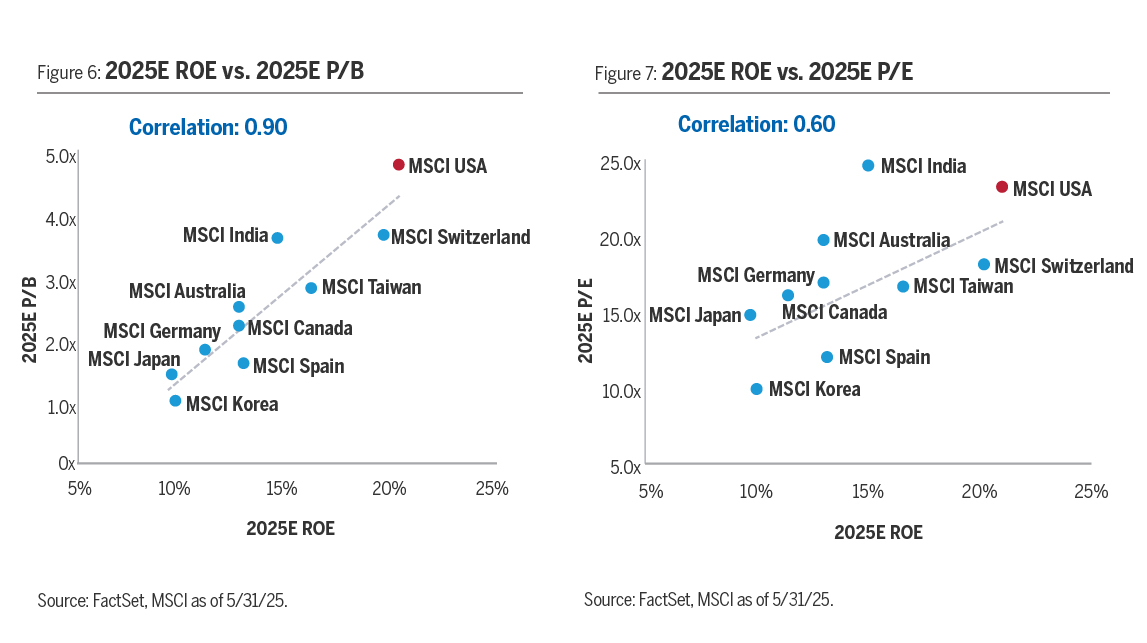

In our view, the relative valuation gap versus the U.S. may begin to narrow as pro-growth policies and capital market reforms outside the United States could drive stronger corporate earnings growth, and potentially stronger returns. For example, Figures 6 and 7 highlight the strong correlation between profitability, measured by return on equity (ROE), and valuations, using both price-to-book (P/B) and (P/E) ratios. In both figures, the red dot representing the MSCI USA Index has the highest ROE relative to other countries, which helps explain the relative valuation premium. As capital efficiency improves, and corporate earnings growth accelerates globally—as observed in the U.S. since the GFC—we believe ROEs across international equity markets should trend higher. Given the strong historical correlation between profitability and valuations, we believe that rising ROEs in international markets should support correspondingly higher valuation multiples.

In summary, allocating to international equities today is about accessing structurally improving markets with attractively-valued growth stocks. Increasingly capital friendly geographies represent an emerging source of compounding earnings growth, rising returns, and improving valuations. For these reasons, we believe that international equities may provide attractive and competitive returns relative to the U.S. for the first time since the GFC.

III. Why It Pays to Go Active

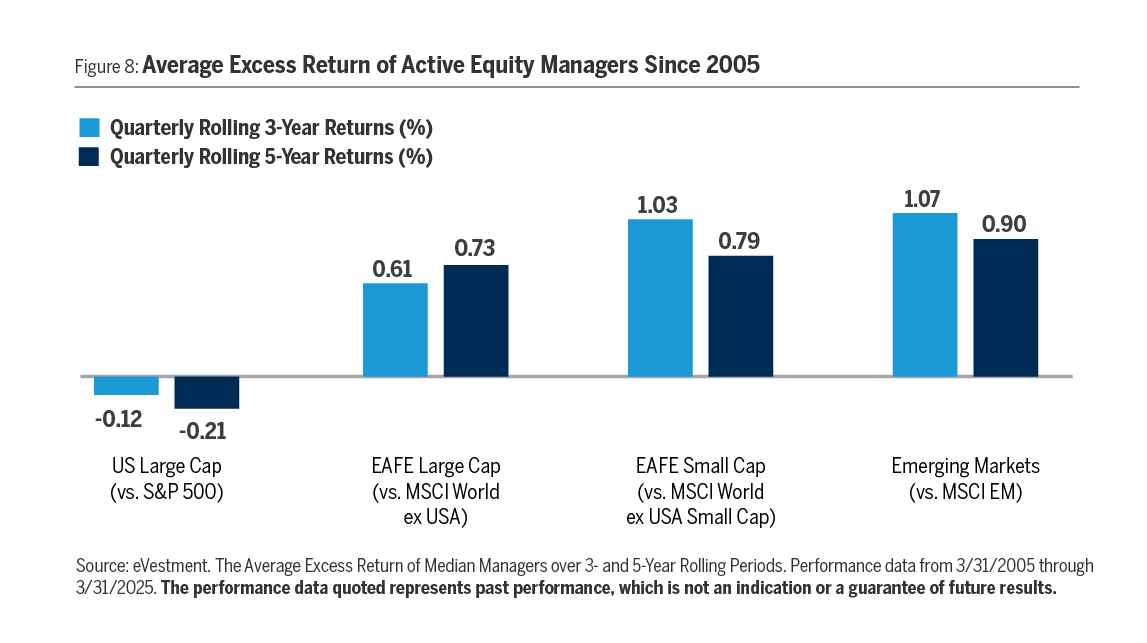

While U.S. passive index funds have dominated headlines in recent years—largely due to their low fees and the relative difficulty active managers face in generating excess returns—active management in international equity markets appears far more compelling. Over the past two decades, the average excess return of active managers within international markets has been significantly higher than the U.S. as measured over rolling three- and five-year periods, where the edge is even greater in international small cap and emerging markets (see Figure 8). At the same time, passive international index funds typically charge three to ten times the average expense ratio of an S&P 500 fund, reflecting the added complexity, lower scale, and inefficiency of non-U.S. equity markets. As a result, fees on passive international products sit close to those of active funds. Given this narrow cost gap and the demonstrably higher alpha opportunity available in less-efficient international markets, we believe that paying a modest premium for skilled active management is sensible—the potential outperformance could more than offset the incremental fee over the long-term.

We believe that one of the primary reasons international and emerging market active managers have generated higher excess performance is a higher level of market inefficiency in ex-U.S. equity markets relative to the U.S. In simple terms, market inefficiency occurs when a security’s price deviates from its true economic value because of information delays, investor psychology or trading frictions. These mispricings create opportunities for disciplined investors to buy undervalued shares or sell overvalued ones. If a market is highly efficient, then the opportunities to buy mispriced assets are scarce, and active managers will likely find it hard to consistently generate alpha. Conversely, highly inefficient markets provide more opportunities for active managers and can make outperformance more feasible.

Taking this one step further, we measure the inefficiency of an equity market with five inputs: 1) number of stocks in the universe, 2) average number of sell-side analysts per stock, 3) level of institutional ownership, 4) frequency of consensus forecast error, and 5) average magnitude of forecast error. Combined, we believe these factors highlight areas where attentive, informed investors can more readily identify attractive investments that others have missed. Based on this definition, international and emerging equity markets demonstrate, on average, higher levels of inefficiency. We believe this helps explain why the average international active manager has historically generated higher excess returns than the average U.S. manager.

The Redwood Investment Framework: Within the broad active investment management space, we believe our approach may be particularly well-suited to non-U.S. markets. While monitoring the global economic backdrop is important for investors, the Redwood investment team primarily focuses on conducting bottom-up fundamental analysis to identify companies with the ability to compound their earnings meaningfully faster than the consensus expectations. We conduct our own due diligence, spending most of our time 1) independently forecasting multi-year earnings growth and 2) evaluating the quality of the business. We then assess the valuation for each individual company based on our independent multi-year earnings forecasts.

1) Misforecasted Earnings Growth: Sell-side forecasts tend to miss their mark, especially when predicting earnings over longer periods. The further analysts try to forecast into the future, the greater their errors tend to be, creating opportunities to invest in companies whose true multi-year earnings potential is underestimated. By constructing our investment team, philosophy, process, and incentive structure appropriately, we can escape the “gravitational pull” of consensus and arrive at independent forecasts of multi-year earnings.

2) Quality: Investors often focus heavily on short-term performance, overlooking great companies with strong long-term growth potential. “Quality” companies, in our view, have a durable competitive advantage, skilled management teams that effectively utilize these strengths, and solid financial health to execute their strategy. In addition to being resilient, such companies typically achieve better-than-average financial outcomes, such as high return on invested capital, strong profit margins, and stable balance sheets. Our experience has found that focusing on quality often leads us to higher levels of conviction in our differentiated view of earnings.

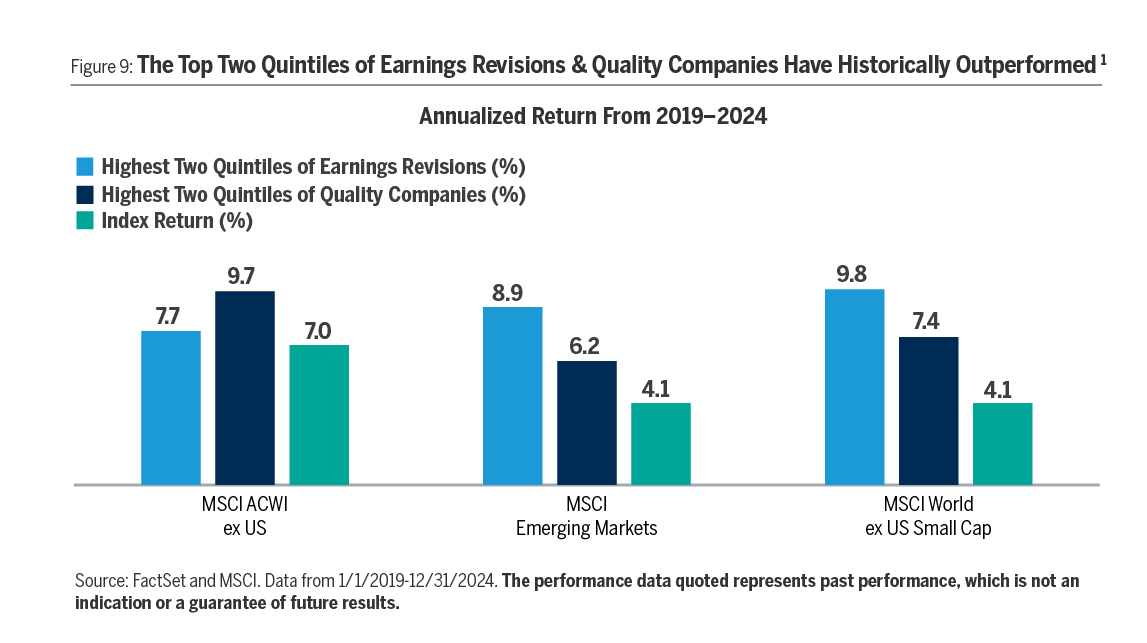

We believe that combining our emphasis on quality businesses with a search for misforecasted earnings growth serves as a reliable investment framework in identifying and owning companies that can compound their earnings faster than the market expects over the medium-to-long term. To validate mis-forecasted earnings and quality as persistent sources of alpha, in Figure 9, we quantify the performance of the two highest quintiles by the quality and earnings revisions factor within the MSCI ACWI ex U.S., MSCI World ex U.S. Small Cap and MSCI Emerging Markets Index. As shown in the chart, the top two quintiles of companies by quality and earnings revision factors outperformed their respective benchmarks over the past five years.

As demonstrated, active management has historically outperformed passive indexing in international and emerging equity markets due to higher market inefficiency. Redwood’s investment approach emphasizes bottom-up fundamental analysis, specifically targeting high-quality businesses with durable competitive advantages and underappreciated earnings growth potential.

Going Forward

In short, while the era of U.S. exceptionalism has been undeniably rewarding for investors since the 2008 GFC, we believe it is prudent to challenge existing assumptions and recognize the pivotal shift in capital friendliness unfolding internationally. The economic momentum the U.S. has enjoyed since the GFC may be slowing amidst growing policy uncertainty, which may remove the strong USD headwinds that hindered international equity performance. Concurrently, the era of capital-friendliness, previously dominated by the United States, is rapidly expanding globally. Structural reforms from Europe to Asia are fostering pro-investment environments by streamlining regulation, stimulating fiscal spending, and encouraging corporate efficiency—key ingredients for unlocking shareholder value. Additionally, powerful secular growth trends in technology, infrastructure, energy, and defense offer compelling opportunities, often overlooked and significantly discounted relative to their U.S. counterparts. In our view, for the first time in many years these conditions present an actionable moment for prudent investors to actively consider portfolio allocation toward international equities. Further, disciplined active managers, adept at identifying high-quality companies poised for robust, underestimated earnings growth, may be uniquely positioned to leverage this global rotation. We believe it is time to overcome the psychological inertia of U.S. exceptionalism, reevaluate traditional investment frameworks, and capitalize decisively on the compelling, yet underappreciated opportunities now unfolding in international equities.