A growing strain of macro commentary argues that artificial intelligence (AI) will drive significant white collar job destruction and broad economic contraction. The bearish narrative posits that as AI replaces large swaths of professional labor, income will fall, consumption will weaken, and GDP will decline.

We do expect meaningful disruption from AI. Certain industries will shed jobs, and some segments of the economy will be materially diminished, creating real economic pain for those affected. In the short to medium term, we anticipate a reallocation of economic activity away from consumption and toward business investment, as AI-driven data centers and infrastructure generate increasing value. During this period, we believe value may accrue disproportionately to capital over labor, as the transition temporarily disrupts the labor force. Over the long term, however, we believe the U.S. economy will once again demonstrate its dynamism, reabsorbing labor, sustaining income growth, and ultimately supporting continued expansion in consumption and overall economic prosperity.

Investment-Driven Growth

Major technological transitions typically begin with a surge in investment spending as capital is deployed to build the new productive infrastructure before legacy sectors fully contract. This investment boom precedes, and helps absorb, the economic disruption that follows by providing a growth engine that does not rely on immediate consumption expansion.

The process is already underway owing to AI. Capital is being directed toward physical infrastructure such as data centers, semiconductor fabrication, power generation and transmission, logistics networks, and other hard assets required to support new capabilities (see also

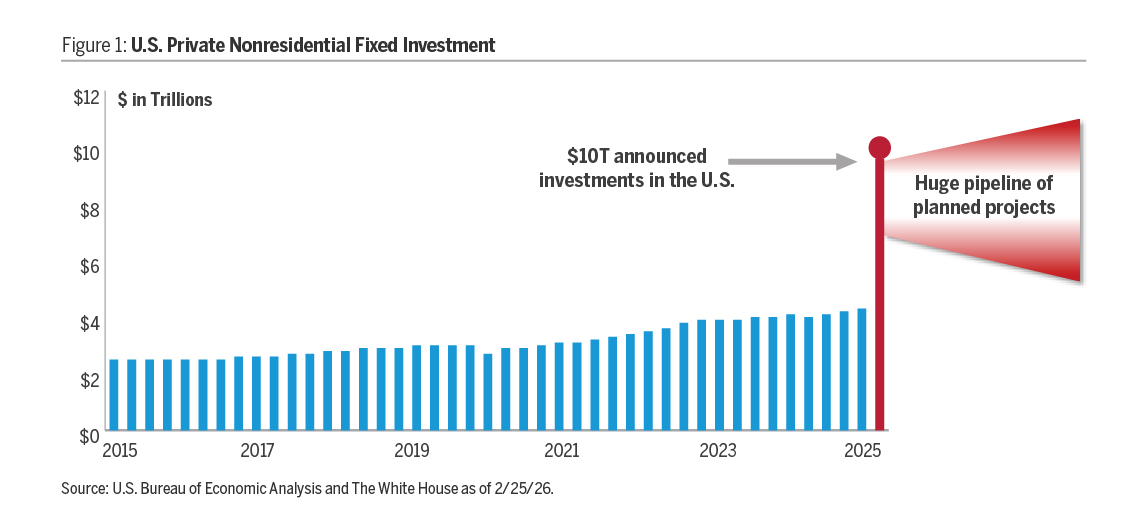

An American Business Spending Boom). This is physical investment, including labor intensive construction, engineering, manufacturing, and logistics, and it counts directly toward economic output. In fact, roughly $10 trillion of private fixed investment has been announced that may create a surge in GDP growth in the years ahead (see Figure 1).

Beyond the buildout of physical infrastructure, firms across industries are already deploying AI to transform their own operations — and the early results suggest that productivity gains are being reinvested, not extracted. J.P. Morgan, for example, has disclosed roughly $2 billion in annual savings from AI investments, including the automation of labor‑intensive “Know Your Customer” processes. At most firms, these savings have not led to organizational contraction, but to the reallocation of resources toward higher‑value activities.

We observe a similar dynamic internally at Alger. AI‑enabled tools have lowered the unit cost of producing client communications, enabling us to increase output and expand investment in distribution and engagement without reducing overall spending.

AI is following the historical pattern of major technological transitions, in which investment and capital formation lead economic change. This dynamic is now clearly visible in the data. Last year, real business investment grew nearly twice as fast as overall GDP, while technology related business spending grew roughly ten times faster, reinforcing the investment led nature of the current cycle. We expect this trend to continue. As a result, we believe portfolios should be positioned to capture business investment broadly, and AI infrastructure in particular, as the core enabler of this transition.

Creative Destruction

Over the long run, the economic effects of AI are best understood through the lens of creative destruction. Renowned economist Joseph Schumpeter described capitalism as a process of creative destruction as the continual dismantling of old economic structures and their replacement with new ones. Major innovation, in this framework, is not additive at the margin, but disruptive by design. It destroys specific firms, industries, and professions even as it expands total productive capacity and long term wealth.

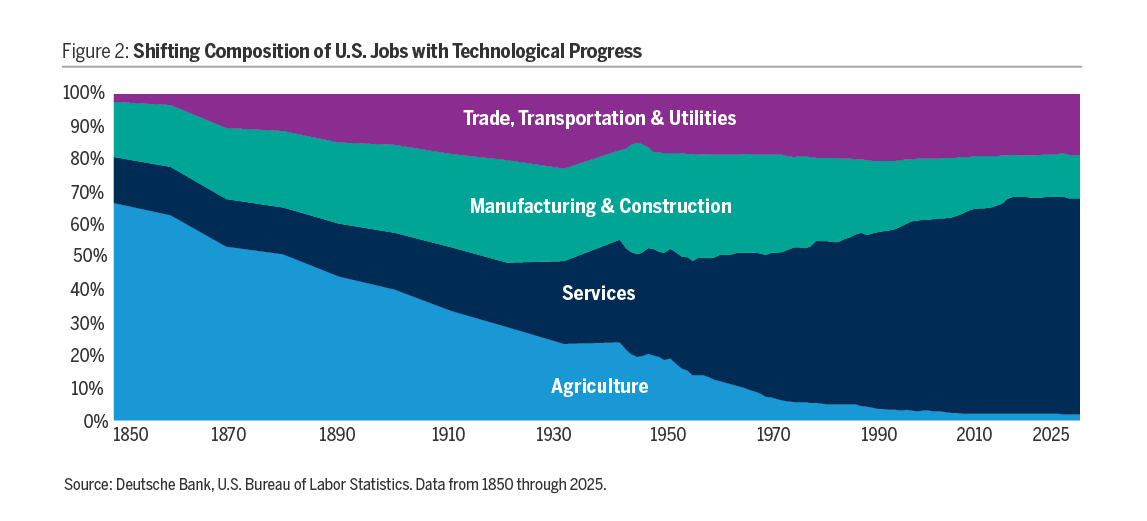

At the turn of the 20th century, roughly 40% of the American workforce was employed in agriculture. However, the advent of mechanization such as tractors and combines allowed a small fraction of that labor force to produce far more than the entire sector had previously. If one had projected forward from that moment, the fear of mass, permanent unemployment would have seemed entirely rational. Where would tens of millions of displaced workers go?

The flaw in the question is that it assumes the future labor market must be visible from the present. It wasn’t. Displaced agricultural workers did not move into roles that already existed. They became factory workers, railroad laborers, miners, machinists, dockworkers, and construction workers as industrialization expanded. Over time, those roles evolved and gave rise to new professions. What began as mill work and rail constructions progressed into engineering, industrial management, electrical trades, logistics, aviation, computing and eventually software (see Figure 2).

This is the core insight of creative destruction: value and labor do not vanish when productivity rises, rather they are reallocated. The economy sheds old forms of work while creating new ones elsewhere, often in places that are impossible to predict in advance.

Value Migrates; It Is Not Destroyed

What the more cautious narratives get right is that value is shifting. Business models built on friction, information asymmetry, or human intermediation face real pressure. Some will not survive. That is the destructive portion of creative destruction.

But destruction at the firm or sector level is not the same thing as destruction at the macro level. The economic surplus that once accrued to legacy software vendors, intermediaries, or labor intensive service models will not disappear; it will be redistributed.

History offers repeated examples of this dynamic. The printing press sharply reduced the cost of producing written material, displacing scribes but vastly expanding the information economy as demand rose for writers, printers, publishers, and educators. The automobile replaced horses and carriage makers, but by dramatically lowering the cost and friction of travel, it unlocked far greater mobility and catalyzed employment across manufacturing, road construction, energy, logistics, insurance, and tourism.

Fears that labor saving technology would leave society permanently worse off are not new. A February 26, 1928 New York Times headline warned that the “march of the machine” was creating “idle hands,” reflecting widespread concern that rising productivity would outpace demand for labor. In hindsight, that fear now reads as profoundly misplaced. The economy adapted, new industries emerged, and employment ultimately expanded as productivity gains were absorbed and redeployed across new forms of economic activity.

We believe a similar process is unfolding today. The economic surplus that once accrued to legacy software vendors, intermediaries, or labor intensive service models will not disappear; it will be redistributed. In our view, it will flow to infrastructure providers, to existing companies and new entrants that can build at radically lower cost, and to consumers who pay less for the same output.

This is precisely how prior innovation cycles expanded the economic pie. Subsistence farming gave way to manufacturing. Manufacturing gave way to services. New categories of consumption such as entertainment, leisure, and digital services emerged only after productivity made them affordable. While it may be tempting to imagine a future in which AI and automation permanently satiate human desires, history suggests the opposite. In the 1790s, a farm laborer spent roughly three quarters of his wages on food, leaving little room for discretionary consumption.

1 Today, Americans spend closer to 13% of their income on food, with much of the remainder directed toward goods and services that either did not exist or were unimaginable in earlier eras, including automobiles, electronics, travel, and recreation.

As productivity rises, human aspirations tend to expand alongside it. In this way, AI driven productivity gains are likely to boost, not reduce, aggregate demand over time.

The New Adopters

In the near term, the most visible winners of the AI cycle are the enablers — the companies providing the infrastructure, compute, power, networking, and tools required to make large scale intelligence possible. That is consistent with prior general purpose technologies: early value accrues to those who build the rails.

Over the longer arc, however, we believe the enduring economic winners could be the adopters. These are the businesses that use the technology to change cost structures, create new products, and reconfigure entire industries. This is how general purpose technologies ultimately compound value. Electricity’s largest value creation did not occur in generation and transmission, but in transforming manufacturing, logistics, consumer goods, and services once firms redesigned processes around cheap, reliable power. The internet followed a similar pattern. Early value accrued to foundational layers such as networking hardware, protocols, and access software, but its greatest economic impact emerged later as businesses redesigned distribution, commerce, and service models around ubiquitous connectivity. Many of the defining internet enabled companies were created years after the web became widely usable, once adoption deepened and business models fully adapted. Uber and the gig economy, for example, emerged more than a decade later.

AI may follow a similar trajectory. ChatGPT’s release in November 2022 was a catalytic moment, not an endpoint, akin to the launch of Netscape’s browser in 1994, which opened the web to mass use but did not determine its eventual economic impact. Many of the most important AI enabled companies likely have not yet been formed, just as the defining internet platforms emerged only after adoption deepened and business models adapted.

For investors, this implies a progression rather than a single moment: infrastructure and enablers lead early, while adopters drive the next phase of value creation.

Conclusion

The disruption is real. Some industries will shrink. Some job categories will not return. Investors should be clear eyed about which business models rely on assumptions about friction, labor costs, or complexity that no longer hold.

However, an overly bearish stance on the economy and equity markets risks underappreciating the gains that have historically accompanied periods of rapid technological change. The process of creative destruction, as described by Schumpeter, has never produced permanent economic impoverishment. It forces painful transitions, dismantles legacy structures and redistributes value and then it expands the economy’s productive frontier.

No one could have predicted the development of software engineering from the vantage point of early 20th century farm labor, and it is difficult to predict the categories of work that widespread intelligence capability will unlock from where we sit today. History suggests, with remarkable consistency, that they will emerge.

But creative destruction produces losers as well as winners. A rising tide of AI-driven productivity will not lift all boats equally. Legacy business models built on friction and manual complexity may erode even as new categories of value expand. For investors, the opportunity lies not in broad market exposure, but in identifying the specific companies pioneering change and positioned to capture disproportionate value as this cycle unfolds.

That is precisely what Alger has done for more than six decades: using deep, fundamental research to identify the innovators reshaping industries — from the PC to the internet to smartphones — and owning them through periods of transformative change. As AI redraws the competitive landscape, we believe that disciplined, research-driven selection will be more important than ever.